Power of Rs. 30,00,000 One-time Investment in Mutual Fund: In how much time can your lump sum investment Generate Rs. 6.3 crore corpus at 12%

The Power of Compounding: Turning ₹30 Lakh into ₹6.3 Crore

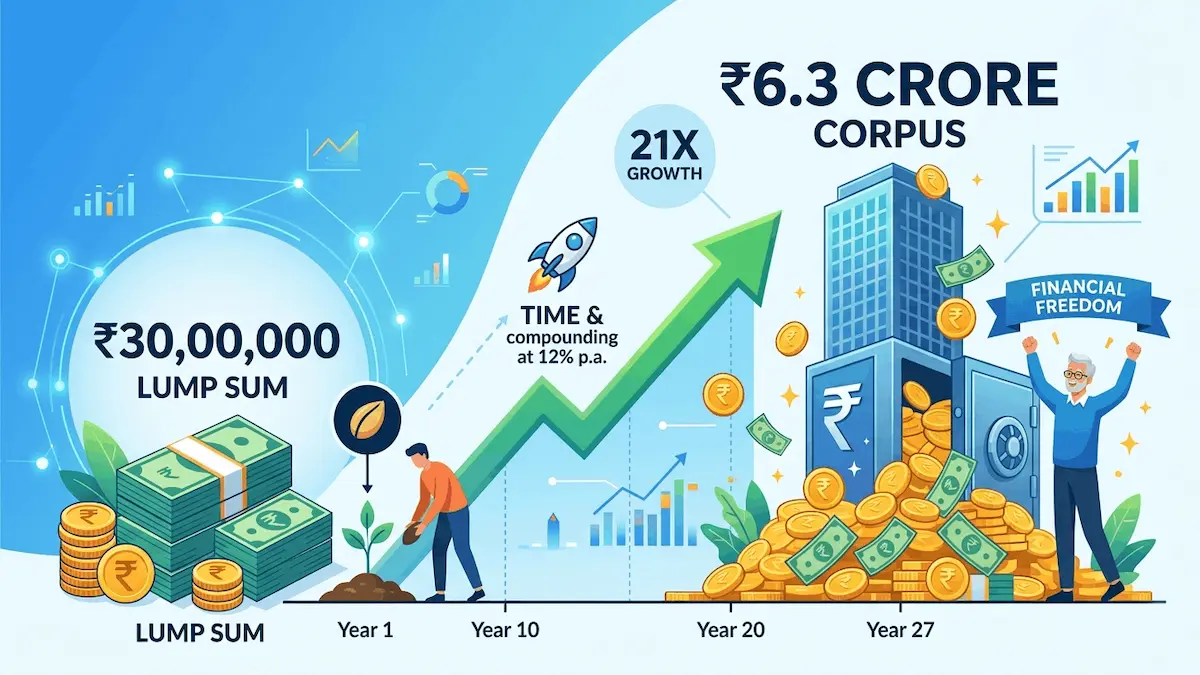

Investing is often seen as a marathon, not a sprint. However, when you have a significant lump sum and the “magic” of compounding on your side, that marathon can lead to a breathtaking finish line. Many investors wonder: Is it actually possible to turn a one-time investment of ₹30,00,000 into a massive ₹6.3 Crore corpus? Power of 30 Lakh Investment

The answer is a resounding yes, provided you have the most valuable asset in the financial world: Time.

In this comprehensive guide, we will break down the math, the strategy, and the patience required to achieve a 21x return on your investment using Mutual Funds. Power of 30 Lakh Investment

The Core Math: How Long Will It Take?

To calculate the time required for a lump sum to grow, we use the formula for Compound Interest:

Where:

$A$ = Final Corpus (₹6,30,00,000)

$P$ = Principal Amount (₹30,00,000)

$r$ = Annual Interest Rate (12% or 0.12)

$n$ = Number of years

When we plug in the numbers for a 12% annual return, the math reveals a specific timeline:

It will take approximately 27 years for your ₹30 Lakh to grow into ₹6.3 Crore.

The Breakdown of Growth

| Investment Milestone | Estimated Time (Years) | Approximate Value |

| Initial Investment | Year 0 | ₹30,00,000 |

| Doubling your money | Year 6 | ₹60,00,000 |

| Reaching ₹1 Crore | Year 11 | ₹1,04,00,000 |

| Crossing ₹3 Crore | Year 21 | ₹3,24,00,000 |

| The Final Goal | Year 27 | ₹6,39,00,000 |

Why 12%? The “Realistic” Sweet Spot

You might wonder why we chose 12% as the benchmark. In the context of the Indian economy and the historical performance of the Nifty 50 or Sensex, 12% is often considered a realistic long-term expectation for diversified equity mutual funds.

While some years might see a 20% gain and others a 5% loss, the long-term average (CAGR) tends to hover around this mark for well-managed aggressive hybrid or large-cap oriented funds. Power of 30 Lakh Investment

The “Magic” of the Last Decade

One of the most fascinating aspects of compounding is that the growth is back-loaded.

Look at the table above again. It takes 11 years just to reach your first ₹1 Crore. However, in the final 6 years (from year 21 to 27), your corpus jumps from ₹3.2 Crore to ₹6.3 Crore. Power of 30 Lakh Investment

You earn more in the last 6 years than you did in the first 21 years combined. This is why “staying in the game” is more important than “timing the market.”

Which Mutual Funds Should You Consider?

To aim for a 12% consistent return over nearly three decades, you cannot play it too safe. Fixed Deposits (FDs) or Gold likely won’t hit these numbers after inflation and taxes. You need exposure to Equity.

1. Index Funds (The Low-Cost Route)

Investing in a Nifty 50 or Nifty Next 50 Index fund ensures you are betting on the growth of India’s top companies. They have low expense ratios, which means more money stays in your pocket to compound.

2. Flexi-Cap Funds

These funds allow fund managers to move between large, mid, and small-cap stocks based on market conditions. This flexibility is ideal for a 25+ year horizon.

3. Aggressive Hybrid Funds

If you are wary of extreme volatility, hybrid funds (which mix equity with a small portion of debt) can provide a smoother ride while still aiming for that 10-12% long-term target. Power of 30 Lakh Investment

The Enemies of Your ₹6.3 Crore Goal

While the math is simple, life is not. To reach this goal, you must defeat three major enemies:

1. The Temptation to Withdraw

At Year 15, your ₹30 Lakh will be worth roughly ₹1.6 Crore. You might be tempted to withdraw it to buy a luxury car or a larger home. If you do, you kill the compounding “engine” before it hits its most productive phase. Power of 30 Lakh Investment

2. Inflation

₹6.3 Crore sounds like a lot today, but in 27 years, its purchasing power will be significantly lower. To combat this, some investors choose to “Top-up” their investment periodically rather than just leaving a one-time lump sum.

3. Taxes (LTCG)

Currently, Long-Term Capital Gains (LTCG) tax on equity is applicable on profits exceeding ₹1.25 Lakh per year. You must factor in that a portion of your final corpus will go to the government.

Strategy: How to Invest ₹30 Lakh Safely

Investing ₹30,00,000 in a single day can be risky if the market crashes the following week. Experts suggest two main approaches:

The Direct Lump Sum: If you have a very long horizon (25+ years), a one-time entry might not matter much in the long run.

Systematic Transfer Plan (STP): Park your ₹30 Lakh in a Liquid Fund and “transfer” a fixed amount (e.g., ₹2 Lakh per month) into your chosen Equity Mutual Fund over 15 months. This averages your purchase cost and protects you from sudden market volatility.

The Psychological Aspect of Wealth Building

The hardest part of turning ₹30 Lakh into ₹6.3 Crore isn’t picking the fund—it’s doing nothing. There will be market crashes, pandemics, and economic recessions. During these times, your ₹30 Lakh might temporarily drop to ₹25 Lakh. Most people panic and sell. To reach the ₹6.3 Crore mark, you must have the stomach to watch your portfolio fluctuate without hitting the “Sell” button.

Conclusion: Is It Worth It?

Achieving a ₹6.3 Crore corpus through a ₹30 Lakh lump sum is a testament to the power of patience. By choosing a diversified mutual fund and allowing it to grow at a 12% CAGR for 27 years, you aren’t just saving money; you are creating generational wealth.

The best time to start was yesterday. The second best time is today. If you have the capital, start your journey, stay disciplined, and let time do the heavy lifting for you. Power of 30 Lakh Investment

Frequently Asked Questions (FAQs)

1. What if I get only 10% returns instead of 12%?

At 10%, your ₹30 Lakh would grow to approximately ₹3.9 Crore in 27 years. Those 2 percentage points make a massive difference of nearly ₹2.4 Crore!

2. Is 27 years too long to wait?

Wealth creation is a slow process. However, if you increase your investment or find funds that return 15%, the time frame can drop significantly (to about 22 years for 15%).

3. Can I lose my principal amount?

In equity mutual funds, there is a risk of capital loss in the short term. However, over a 20-30 year period, the probability of the Indian stock market being lower than it is today is historically very low. Power of 30 Lakh Investment

Disclaimer

Investment in Mutual Funds is subject to market risks. Please read all scheme-related documents carefully before investing. The calculations provided in this article are based on an assumed annual return of 12% and are intended for illustrative purposes only. Past performance is not an indicator of future results. It is highly recommended to consult with a SEBI-registered financial advisor before making large financial decisions.

Read Also ↓

Cyber Liability Insurance 2026: The Ultimate Shield for Every Digital Business! | Business Insurance for Small Business: A Complete Guide to Protecting Your Assets in 2026 |